What makes mortgage lending in Hawaii different?

The residential mortgage market in Hawaii is unlike any other in the country. As one of the most beautiful places in the world full of amazing people & culture, it is a desirable place to live, own a second home, or an investment property. Navigating the residential mortgage market can be difficult for borrowers, so borrowers seeking a residential mortgage in Hawaii need a trusted advisor with the knowledge and experience to guide them through its peculiarities. Choosing a Hawaii based bank familiar with the nuances that make residential mortgage lending in Hawaii unique as well as the programs to accommodate Hawaii’s many atypical homes is generally a great option for borrowers. This article strives to educate borrowers so that they can make informed and successful decisions when it comes to making one of the largest financial transactions of their lives.

There only 4 large Hawaii based banks, whereas on the US Mainland most large metropolitan areas are served by many more than just 4. In Hawaii these banks are Central Pacific Bank, American Savings Banks, First Hawaiian Bank, and Bank of Hawaii. Though Bank of Hawaii holds the most money in terms of checking and savings accounts, Central Pacific Bank consistently funds more purchase mortgages than anyone else in the state. Though less common, a borrower can also get a mortgage in Hawaii through a credit union, independent mortgage broker, correspondent lender, or non-Hawaii based bank like Bank of America or Wells Fargo which do not have branches in Hawaii.

Although a borrower can get a residential mortgage loan from a large Mainland bank like Bank of America or Wells Fargo, these institutions do not have bank branches in Hawaii, so borrowers are regulated to calling these companies over the phone for service, or they are required to go online to pay their bill. In contrast, by getting a mortgage through a locally based Hawaiian bank a borrower can walk into a branch for service or to get billing issues resolved. Though many of these large Mainland banks have tried opening branches in Hawaii, their attempts have been defeated by expensive overhead such as commercial space and traveling, logistical challenges such as time zone differences and physical separation, and a Hawaiian culture that has a deep seeded preference toward working with locally owned and or locally operated companies instead of large Mainland corporations.

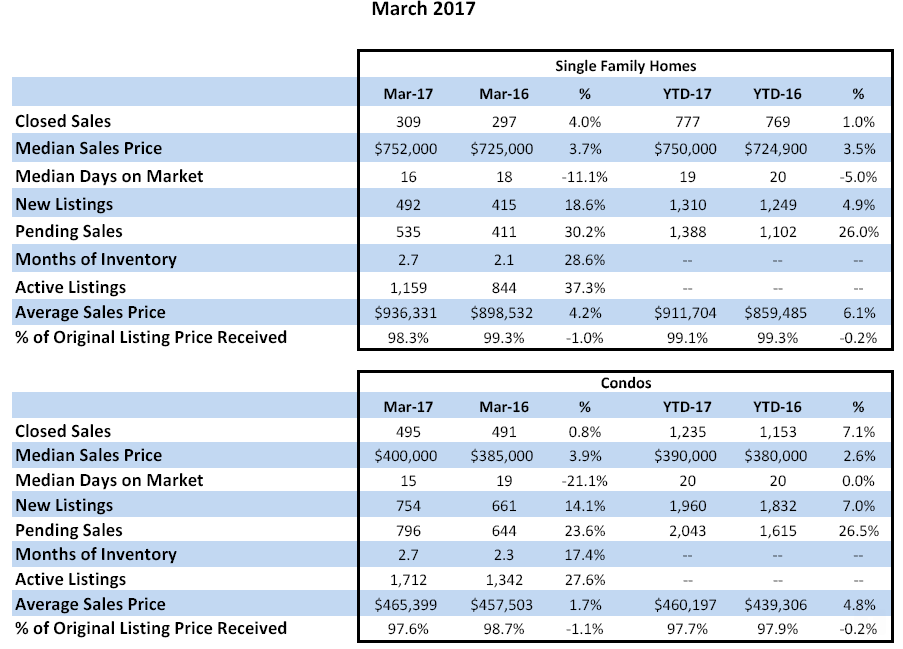

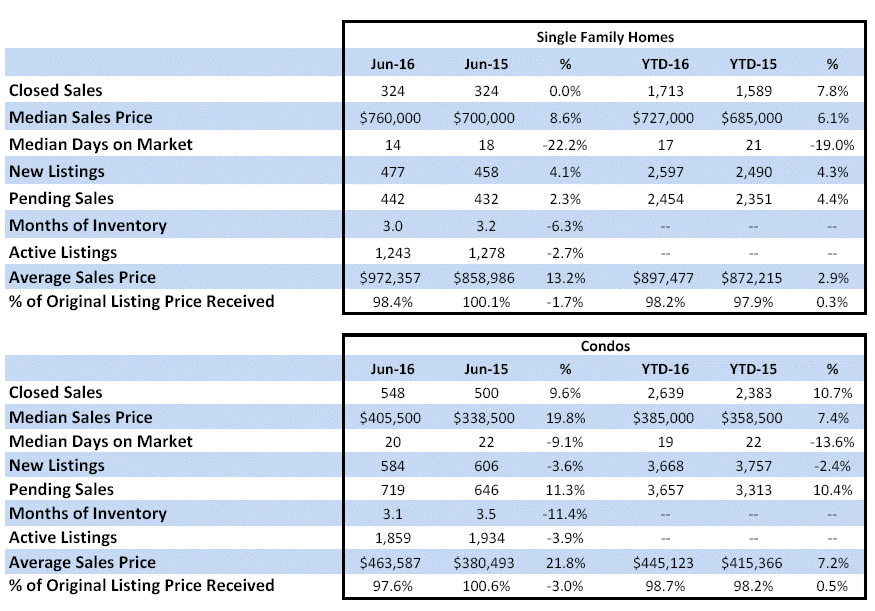

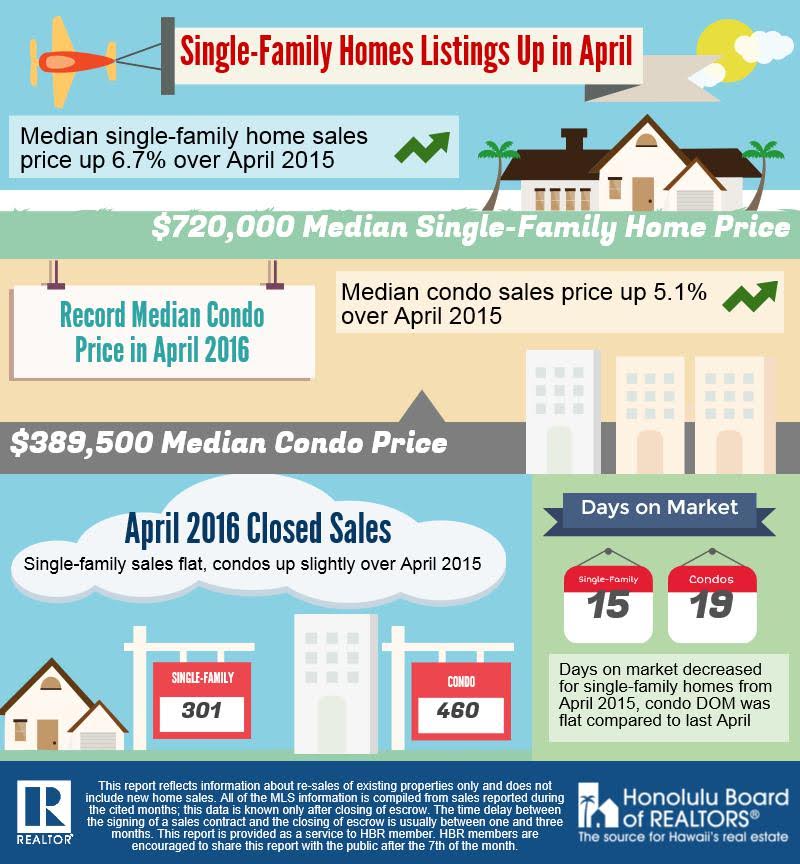

It is no secret that Hawaii has a high cost of living, particularly for housing. In Honolulu county in April 2016 the median price for a single family residence was $720,000 and the average sales price was $933,044. This compares to an average median home price for the US on the whole of $222,700. Materials to build homes are more expensive in Hawaii due to shipping costs. The talent pool for skilled labor able to build quality homes is also smaller in Hawaii. The extraordinary high cost for housing has led to a high rate of single family homes being converted to multi-family dwellings. For example, an individual may buy a 2000 square foot home and divide up the home into two 1000 square foot living spaces. It is not uncommon for this to be done by the owner without obtaining the proper permits from the City and County. It is also not uncommon for the washer and dryer to be outside the home on the side of the house, an extra toilet to be in the garage, an additional shower installed in the backyard, etc.. Many non-Hawaii based lenders will refuse to issue a mortgage on a property with these kinds of unique unpermitted or non-conforming grandfathered in features, and many time buyers will pay $600 to $1100 for an appraisal only to have their mortgage loan denied. However, most local banks understand that homes with these features are common in Hawaii and are comfortable lending on them.

Hawaii housing developers also commonly choose to zone properties as a Condominium Property Regime (CPR). These are more commonly referred to as detached condo’s on the Mainland, and are rare in the US other than Hawaii. When standing on the sidewalk and looking at the home you could not tell if the home was zoned as a single family residence or as a CPR. But by choosing this kind of zoning and property type prior to construction, then builders can reduce costs and sometimes speed up the building process. The downside is that these properties are technically condominiums that have their own bylaws, association, HOA dues, and common areas, however projects with 4 units or less typically don’t hold formal association meetings or collect HOA dues, instead each owner buys their own hazard insurance and mows the lawn around their house. Owners each have equal ownership interest in the land under the entire project and common areas, and owners will likely need to deal with the other owners in the project on matters over time. Non-Hawaii based lenders see CPR’s infrequently, and they commonly place unneeded lending restrictions on these kinds of properties. Since there can be additional lending restrictions on these properties as well as the fact that all owners have equal percentage ownership interest in the land the project sits on, as opposed to outright ownership of the land as is the case for single family homes, CPR’s are valued slightly less than an equivalent single family home.

Condominiums are an attractive option for many buyers as the median sales price is significantly less than the median sales price of a single family home. In Honolulu county in April 2016 the median sales price for a condominium was $389,500 and the average sales price was $462,803. However, buyers often fail to consider the high cost of HOA dues, which for the most part ranges from 60 cents to 90 cents per square foot, depending on the services and amenities of the condo building, meaning for a 1000 square foot condo you can expect to pay somewhere between $600 and $900 per month in HOA dues on top of your mortgage, taxes, and insurance. HOA dues virtually never go down, and instead go up at least at the pace of inflation, if not faster when budgeted costs increase faster than expected. Older condo projects consistently have expensive repairs that can create the need for special assessments as well. A down side of owning a condominium is that you are much more restricted in what you can do with your property, which can come down to small things like what color your blinds and curtains are allowed to be. However, the upside is that you don’t have the typical responsibilities of a home owner, such as mowing your lawn; paying for trash, water, and sewer; and fixing things like your roof when it is damaged.

Hawaii is a state that allows for accommodation mortgagors. This where a person is on title to the property who is not on the loan. A common example is when a husband takes out a mortgage to buy a property, and his spouse is not on the loan, but they take title to the property jointly as husband and wife. A Hawaii based lender will generally allow for a non-married person to also be on title to a property even though that person is not on the loan. A common example is where parents take out a mortgage, and add their children to title even though the children are not not the mortgage loan. A non-Hawaii based lender may not allow for this, which can be inconvenient during certain estate planning situations. If the lender does allow for this, then the accommodation mortgagor will generally be required to sign certain documents like the mortgage, notice of right to cancel, and a few others.

When it comes time to record your Hawaii residential mortgage loan, then your mortgage and conveyance documents will be recorded at one of two recording bureaus – The Regular System Recording Bureau or the Land Court Bureau. Both bureaus take 2 days to record mortgages, whereas the majority of the continental US takes no more than 1 day to record mortgages. These two bureaus serve the entire state, regardless of what county your property is in. One of the nuances with Land Court is that Land Court requires your full middle name to be on title to the property. It will not accept middle initials, whereas the Regular System does not have this requirement. Another difference between the two bureaus is that to change your name on title due to a marriage, for example, or to change vesting from single man to married man, then Land Court requires that you submit a petition for them to record the change, whereas the Regular System would require a standard conveyance deed like the rest of the country. Another quirk of Land Court is that if there is a non-borrowing spouse, vesting must be taken as “John James Doe, husband of Jane Mary Doe”, whereas the Regular System and the rest of the US would allow vesting to be taken as “John James Doe, a married man”.

Hula Mea loans are currently not available as of the time of this writing, however, when they are available, they are great loans for first time home buyers. It’s a program put on by the Hawaii Housing Finance & Development Corporation (HHFDC) for first-time homebuyers, Hawaii residents, US citizens over 18 years old, and who haven’t already received a Hula Mea loan. There are also restrictions on the how much income you can make annually and how expensive the home you intend to purchase can be. These loans are attractive because they offer below market interest rates. When this program is available, then the HHFDC requires potential borrowers must work with a locally based lending institution.

The Department of Financial Institutions (DFI) ensures the safety and soundness of state-chartered and state-licensed financial institutions, including banks that issue residential mortgage loans, mortgage servicers, mortgage loan originators and mortgage loan originator companies. Should you have a compliant about a mortgage lender or servicer, you can file a compliant here: http://cca.hawaii.gov/dfi/.

Hawaii based lenders are familiar with the intricacies of Hawaii residential mortgage lending, which are unique to Hawaii and unlike much of the rest of the United States. Many times, the consequences of using an out of state lender is your purchase or refinance transaction may not close, and you end up wasting a lot of time and money. The risk is so high that many real estate agents will advise sellers to not accept purchase contract offers from a buyer using a non-Hawaii based lending institution, or they will accept one purchase offer over another where the only difference is one used a Hawaii based lender and the other one didn’t. Taking it one step further, Hawaii based banks that have a network of branches are typically the optimum choice for borrowers because these banks use their own money to fund, makes their own underwriting decisions, and have competitive pricing not available to correspondent lenders and mortgage brokers. In addition, the loan is processed, docs are drawn, and funding of the loan all occur in Hawaii by people who are familiar with property and recording bureau peculiarities, which can be the difference of your loan funding or not. This makes working with a Hawaii based bank the choice of people in the know.